Markets have always swung between excitement and disappointment. Prices may climb on a compelling story, then correct sharply when expectations outrun reality. Behavioural finance—the study of how psychological tendencies and emotions might influence financial decisions and market outcomes—helps explain why otherwise savvy investors could get swept up in these waves.

Table of contents

- The classic arc of a bubble

- From tulip mania to modern markets

- Why investors get swept up

- What might help investors

The classic arc of a bubble

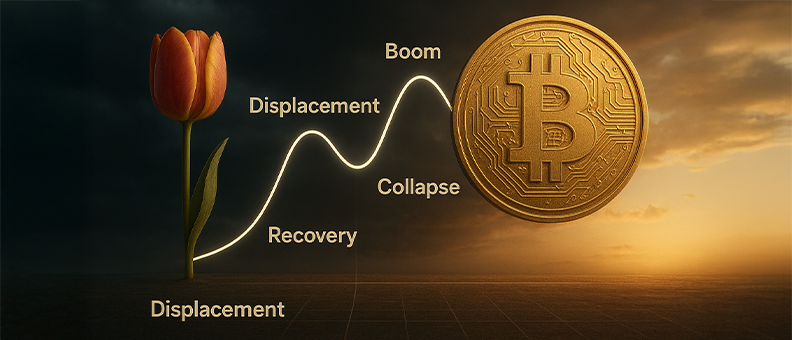

Economists have long described a stylised pattern in speculative episodes. One well-known framework—drawing on the work of Hyman Minsky and elaborated by Charles Kindleberger—identifies five stages: displacement (a new technology, policy, or shock attracts attention), boom (rising prices and broader participation), euphoria (valuation narratives overshadow fundamentals), profit-taking (some early investors begin selling), and panic (selling cascades). Not every rally follows this arc, but when the sequence becomes visible, it may signal elevated risk.

Read Also: What causes a stock market crash?

From tulip mania to modern markets

Seventeenth-century tulip mania in the Netherlands is often cited as one of the earliest speculative episodes. Rare bulbs briefly fetched extraordinary prices before the market broke in 1637. While some popular accounts exaggerate the impact on the Dutch economy, historians agree there was a short, intense boom in tulip bulb contracts that ended abruptly.

Since then, markets around the world have seen similar cycles play out in different forms:

- The US housing bubble (2000s): Home prices rose sharply in the 2000s, aided by easy credit and mortgage securitization. Indices peaked around 2006 and then declined, triggering significant losses across mortgage markets. That housing downturn was an important factor in the 2008 financial crisis. Investor behaviour may have contributed: overconfidence in continuously rising property values and herding around securitized vehicles amplified the rise and fall.

- The dot-com bubble (late 1990s): The Nasdaq Composite peaked in March 2000 before dropping steeply by late 2002, as many internet firms lacking sustainable earnings models collapsed. Investor behaviour may have been shaped by representativeness and recency bias, leading some to assume that all internet companies would replicate the success of early winners, causing the bubble.

- Tech valuations in the 2010s and 2020–21: Beyond the dot-com era, investors piled into new-age tech firms, many of which had yet to turn a profit. While several companies built lasting businesses, valuations in some sectors. Beliefs such as “tech will always dominate” reflect narrative bias at work.

- India’s stock market episodes: The Harshad Mehta securities scam in 1992 drove up prices artificially before collapsing when the manipulation was exposed. India’s real estate surge in the mid-2000s also mirrored global excess, cooling after the financial crisis. More recently, IPO waves in 2017 and 2021 showed pockets of exuberance, though outcomes varied across companies.

- Cryptocurrency cycles: Cryptocurrencies have seen repeated booms and busts. Research finds that surges in bitcoin prices often precede waves of retail adoption, while sharp downturns have left many investors nursing losses. Herding and extrapolation are frequently cited behavioural drivers.

Read Also: Recency Bias & Herd Behaviour in Bull Markets

Why investors get swept up

Behavioural finance points to several robust, research-backed tendencies:

- Herding and information cascades. When people see others buying, they might infer “those buyers know something,” and follow the crowd even if their own information is thin—especially in fast-moving markets. Formal models show how rational individuals could still end up imitating one another, amplifying swings.

- Extrapolation and representativeness. Investors may project recent high returns too far into the future, giving excessive weight to vivid success stories (Past performance may or may not be sustained in future). Seminal work links such sentiment to patterns of overreaction and subsequent reversals.

- Overconfidence and new metrics. In euphoric phases, narratives might justify sky-high prices (“this time is different”) and downplay fundamental anchors—an idea explored in the literature on speculative episodes and popularised in work on “irrational exuberance.”

These tendencies do not mean prices are always wrong; innovation can create value. The point is that psychology may amplify cycles around genuine breakthroughs, stretching valuations beyond what later earnings can support.

Read Also: Impact of Behavioural Finance on Market Conditions

What might help investors

There is no foolproof way to spot bubbles in real time, but a few practices could improve decision quality:

- Interrogate the “displacement.” Big ideas (from railways to the internet to blockchains) can be transformative, yet adoption curves and cash flows may take longer than stories suggest. Mapping how value might reach shareholders could keep expectations grounded.

- Watch participation and funding conditions. Rapid retail entry, ease of financing, and the spread of new valuation metrics may be signals that narratives are running ahead of fundamentals. Evidence from crypto user surges after price spikes is one such indicator to monitor with care.

- Counter common biases. Pre-commitment tools (such as rebalancing rules), diversification, and scenario analysis may help temper extrapolation and herding. None of these guarantees success, but they might reduce the odds of concentrated exposure at euphoric peaks. (The herding literature cautions how quickly cascades can form.)

- Seek multiple reference points. Comparing narrative-driven metrics with cash-flow-based measures, industry capacity data, or historical analogues could reveal gaps between story and substance.

Bubbles are as much about human behaviour as they are about technology or money. Recognising the patterns—and the biases that might fuel them—may not eliminate risk, but it could help investors stay more deliberate when excitement and overconfidence take over the market.

At Bajaj Finserv AMC, we recognise that emotions are the cornerstone of investor behaviour – not just for investors but for investment professionals too. That’s why, behavioural finance is at the heart of our investment philosophy, InQuBe, which combines the Information Edge, Quantitative Edge and Behavioural Edge. By understanding, tracking and monitoring market sentiments and our own investment biases, we seek to make mindful and strategic investment decisions. Get the Behavioural edge by investing with Bajaj Finserv AMC. Read more about InQuBe here.