If you have ever tried to balance your portfolio on your own, you would know it can be difficult. You may start with a detailed plan but may not have the necessary time or the expertise to monitor and adjust your portfolio regularly. Over time, your equity allocation may drift, and your portfolio may move away from your intended mix.

SEBI’s new Life Cycle Fund category offers a structured way to approach this process by building the rebalancing mechanism into the fund itself, using a predefined glide path and a fixed maturity aligned with goal-based investing.

Table of Contents:

- What is a Life Cycle Fund?

- How do Life Cycle Funds work?

- Benefits of investing in Life Cycle Funds

- Example of Life Cycle Fund allocation

- Should you invest in a Life Cycle Fund?

- Who should invest in Life Cycle Funds?

- Limitations of Life Cycle Funds

- How to invest in Life Cycle Funds

What is a Life Cycle Fund?

The Life Cycle Fund category was launched in February 2026, when the regulator issued its Categorization and Rationalization of Mutual Fund Schemes circular.

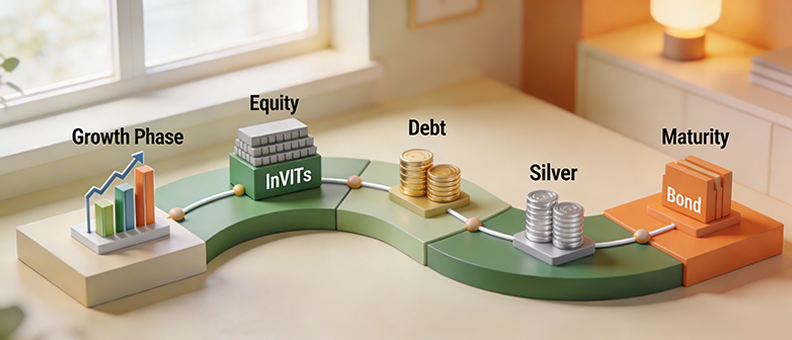

Life Cycle Funds are schemes that follow a glide path strategy across various asset classes such as equity, debt, InvITs, ETCDs, and gold and silver ETFs. These schemes have a predetermined maturity and a predefined asset allocation strategy. Allocation gradually shifts away from equities and towards debt as the fund moves closer to maturity. Think of it as a structured ‘start with growth potential, end with relative stability’ approach, where gradual risk reduction is an integral part of the product design.

How do Life Cycle Funds work?

Life Cycle Funds have four building blocks.

- Predetermined maturity: The scheme follows a pre-defined maturity structure as specified in the Scheme Information Document. This structure may align better with goal-planning than that of other open‑ended funds that do not have a specific tenure.

- Tenure options: Life Cycle Funds can have a tenure ranging from 5 to 30 years, with options available in 5-year increments (5, 10, 15, 20, 25, and 30 years).

- Glide path: The fund follows a scheduled change in asset allocation as time progresses. Typically, this means higher equity exposure in the earlier years and higher debt or defensive exposure as it approaches maturity. The allocation ranges for different stages are defined within SEBI’s framework for this category.

- Multi-asset toolkit: Instead of being limited to just equity and debt, this category allows exposure to additional assets such as gold and silver ETFs, as well as InvITs and ETCDs, within the scheme design.

Benefits of investing in Life Cycle Funds

- You get built-in risk reduction over time. The glide path makes the portfolio more conservative as maturity approaches, saving you the need to rebalance manually.

- Matches goal-based investing: A predetermined maturity can make your goal timeline clearer, especially for medium‑ to long‑term goals such as a child’s education, a house down‑payment window, or a planned retirement milestone.

- It reduces behavioural mistakes. Many investors take more risks when they feel confident and become overcautious after markets fall. A rules‑based glide path helps reduce the risk of emotional decision-making.

- It gives multi-asset diversification in one wrapper. You gain exposure to equity, debt and other specified asset classes without having to manage multiple funds yourself.

- It simplifies monitoring. You can choose one fund for one goal, rather than managing several funds with separate rebalancing schedules.

Example of Life Cycle Fund allocation

Life Cycle Funds with longer maturities have a higher permitted equity allocation in the initial years because the investment horizon is longer, while shorter-maturity options such as 10-year or 5-year funds usually start with a comparatively lower equity exposure and move toward stability sooner.

Here is an example to help you visualise how a glide path may look for a Life Cycle Fund with a 10‑year maturity. This is an illustration for understanding – different Life Cycle Funds may follow different allocations within the permitted regulatory ranges.

Years 1–5

- Equity: 65%

- Debt: 35%

- Gold, silver ETFs and other permitted assets: 10%

Years 5–7

- Equity: 50%

- Debt: 40%

- Gold and silver ETFs and other permitted assets: 10%

Years 7–9

- Equity: 35%

- Debt: 55%

- Gold and silver ETFs and other permitted assets: 10%

Year 10

- Equity: 20%

- Debt: 65%

- Gold and silver ETFs and other permitted assets: 10%

As this example shows, the portfolio moves from growth‑oriented to stability‑oriented as you near maturity, which is the core idea behind glide‑path investing in this category.

Also Read: What Are Thematic Funds – Meaning, Benefits and factors

Should you invest in a Life Cycle Fund?

You may consider a Life Cycle Fund if you prefer a disciplined investment structure and do not wish to actively manage asset allocation yourself. If your goal is time-bound and you favour a “set a plan and follow it” approach, this category is designed to support that style of investing.

It may also suit investors who prioritise progressing toward a financial goal with a managed level of risk, rather than seeking higher return potential at every stage of the market cycle.

However, if you are comfortable rebalancing your portfolio independently and prefer to actively manage shifts between equity and debt, you may not require this structure. Investors with a very high risk appetite may also prefer pure equity funds when their goals are far away, as the defined and range-bound allocation pattern of Life Cycle Funds could feel somewhat restrictive.

Who should invest in Life Cycle Funds?

- Goal‑based investors who want one product aligned to a single timeline.

- Long‑term investors who do not want to manage rebalancing.

- Investors who want a smoother experience as the goal date approaches and prefer not to hold equity‑heavy exposure towards the end of their tenure.

- Investors seeking multi‑asset exposure without creating or managing a complicated portfolio.

Limitations of Life Cycle Funds

- You still face market risk. A glide path is designed to reduce equity exposure over time, but it cannot eliminate drawdowns, especially early in the fund’s life when equity allocation is higher.

- One glide path cannot suit everyone. Your income stability, emergency fund, and personal risk tolerance may not align with the fund’s built‑in timeline.

- Liquidity management: A predetermined maturity improves goal alignment, subject to the scheme’s liquidity terms, but you still need to read the exit and redemption mechanics carefully.

- You may feel constrained in bull markets. As the fund moves towards a higher debt allocation near maturity, it may underperform equity‑heavy options during late‑cycle rallies, and this trade‑off is part of choosing stability.

Also Read: What are consumption funds and who should invest in them?

How to invest in Life Cycle Funds

- Choose the goal first. Decide what you are investing for and the year in which you will need the money.

- Match the fund’s maturity to your timeline. A 10‑year maturity product may not suit a 5‑year goal. The timeline is the crux of this category.

- Read the glide path design. Look at how equity reduces over time, the permitted ranges, and how frequently the fund rebalances.

- Check the asset universe. Since the category may include assets beyond equity and debt, verify how much and when those exposures are allowed.

- Use SIP for behaviour control. If you are worried about timing the market, a SIP into the fund can help you stay consistent during volatile phases.

- Review annually, not daily. Your advantage with this category comes from letting the glide path do its job, rather than reacting to every short‑term movement.

Conclusion

SEBI’s Life Cycle Fund category caters to an important investor need. The time, effort and market knowledge required for manual rebalancing may not suit every investor. Moreover, ensuring a portfolio’s alignment with one’s risk appetite and investment horizon is an essential part of goal-planning. A glide path fund with a pre-determined maturity turns this process into a documented fund design. Such funds typically aim to participate in growth during the early years of investing and gradually reduce risk as the investment horizon shortens. This phased shift in asset allocation may help investors stay aligned with their long-term goals, especially for those who may find it difficult to adjust their portfolios over time on their own.

FAQs

What is the difference between a mutual fund and a Life Cycle Fund?

A Life Cycle Fund is still a mutual fund, but it is a specific category designed to follow a glide path and move across asset classes with a predetermined maturity for goal‑based investing.

What is the meaning of Life Cycle Fund?

A Life Cycle Fund means a fund that changes its asset allocation over time through a glide path, usually becoming more conservative as it approaches maturity.

Are Life Cycle Funds good?

Life Cycle Funds may be suitable for you if you want goal‑based investing with a structured risk‑reduction path and do not want to manage rebalancing yourself. They are not ideal if you want full flexibility or cannot commit to the fund’s timeline.

What is a Life Cycle Fund breakdown?

A Life Cycle Fund breakdown refers to the split of assets such as equity, debt, and other permitted assets at different stages of the fund’s life, based on the glide path defined by the scheme.

Are Life cycle Funds safe?

They are not risk-free. They aim to reduce risk over time by shifting allocations but returns and drawdowns still depend on market conditions and execution.

Should you invest in Life Cycle Funds?

You may consider investing if you have a time‑bound goal and prefer a built‑in glide path rather than manual rebalancing.

Are Life Cycle Funds more aggressive in their asset allocation initially?

Yes, that is typically the idea behind a glide path. Early stages are usually more growth-oriented, and the fund gradually reduces risk as maturity approaches.