Table of Contents

When analysing a company’s market capitalisation, the calculation may appear straightforward: the share price multiplied by the total number of outstanding shares. However, stotal market capitalisation does not always reflect how many shares are actually available for trading in the market.

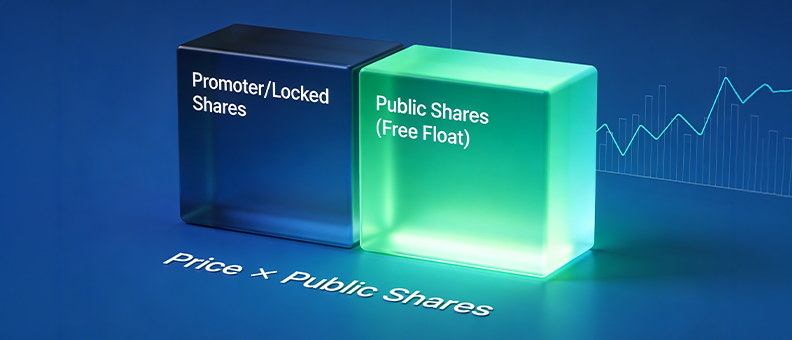

This is where free-float market capitalisation becomes relevant. It considers only the shares available for public trading, excluding promoter holdings and other restricted shares. As a result, it provides a more practical view of a company’s investable market value and liquidity.

In India, major benchmark indices such as the Nifty 50 and the BSE Sensex use the free-float market capitalisation method for index construction and stock weight allocation. As a result, investors in index funds and ETFs are indirectly influenced by free-float methodology even without actively calculating it.

What is free float market capitalisation?

Free-float market capitalisation is the market value of a company’s publicly traded shares that are available for trading on a stock exchange. Unlike total market capitalisation, which includes all outstanding shares, free-float market capitalisation excludes shares that are not normally available for public trading.

These excluded shares may include holdings of promoters, founders, strategic investors, certain government entities, employee welfare trusts, and shares subject to lock-in restrictions. As a result, free-float market capitalisation is generally lower than a company’s total market capitalisation.

Also known as float-adjusted market capitalisation, this method focuses only on shares held by public investors and provides a representation of the company’s publicly tradable market value.

What are some examples of free-float market capitalisation?

Let’s see how free-float market capitalisation works with a simple example.

Example 1: A company with high promoter ownership

Imagine Priya is analysing ABC Technologies, a listed company with:

- 10 crore outstanding shares

- Share price of ₹100

- Promoters holding 60% of the shares

First, she calculates the total market capitalisation:

Total market capitalisation = 10 crore × ₹100 = ₹1,000 crore

However, since promoters own 60% of the company, only 40% of the shares are available for public trading.

Free-float shares = 40% of 10 crore = 4 crore shares

So, the free-float market capitalisation would be:

Free-float market capitalisation = 4 crore × ₹100 = ₹400 crore

While the company’s total market value is ₹1,000 crore, only ₹400 crore represents publicly traded shares available to investors in the stock market.

Example 2: A company with a larger public float

Now consider XYZ Industries, where Raj notices the following:

- 50 crore outstanding shares

- Share price of ₹200

- Promoter and strategic investor holdings of 25%

The total market capitalisation is:

50 crore × ₹200 = ₹10,000 crore

Since 75% of the shares are held by public investors and available for trading:

Free-float shares = 37.5 crore shares

Therefore:

Free-float market capitalisation = ₹10,000 crore × 0.75 = ₹7,500 crore

In this case, the gap between total market capitalisation and free-float market capitalisation is smaller because a larger proportion of shares is publicly traded.

These examples show that two companies can have large market capitalisations, but their free-float market capitalisations may differ significantly depending on how many shares are actually available for trading in the market.

The figures shown are for illustrative purpose only

Total market capitalisation vs free-float market capitalisation: Key differences

While both metrics measure a company’s market value, the key difference lies in the shares considered for the calculation:

| Basis of comparison | Total market capitalisation | Free-float market capitalisation |

| Definition | The total value of all outstanding shares of a company. | The value of only those shares that are available for public trading. |

| Shares considered | Includes all outstanding shares, regardless of ownership. | Includes only publicly traded shares. |

| Shares excluded | No shares are excluded. | Excludes promoter holdings, strategic investments, certain government holdings, employee welfare trusts, and locked-in shares. |

| Calculation | Share price × Total outstanding shares | Share price × Free-float shares |

| Market representation | Reflects the company’s overall valuation. | Reflects the company’s tradable market value. |

| Liquidity indication | Does not indicate how many shares are available for trading. | Provides a better view of shares available for trading and market liquidity. |

| Use in stock indices | Not commonly used for weighting major Indian indices. | Used for index construction and stock weighting in indices such as the Nifty 50 and Sensex. |

Example

Suppose a company has:

- 10 crore outstanding shares

- Share price of ₹500

- Promoter holding of 70%

Total market capitalisation

- = 10 crore × ₹500

- = ₹5,000 crore

Since only 30% of the shares are publicly traded:

Free-float shares

= 3 crore shares

Free-float market capitalisation

= 3 crore × ₹500

= ₹1,500 crore

This example shows that a company can have a large total market capitalisation, but a significantly lower free-float market capitalisation if a substantial portion of its shares is held by promoters or other non-public shareholders.

The figures shown are for illustrative purpose only

Also Read: What Is Market Value? Meaning, Importance & Examples

Understanding the free-float factor

The free-float factor (also known as the float factor) represents the proportion of a company’s outstanding shares that are available for trading in the stock market. It helps distinguish between the total number of shares issued by a company and the shares that are actually accessible to public investors.

When calculating the free float, shares held by promoters, founders, government entities, strategic investors, employee welfare trusts, and other locked-in shareholders are typically excluded because they are not regularly traded in the market. The remaining shares are known as free-float shares.

The free-float factor is expressed as a decimal and is calculated using the following formula:

Free-float factor = Free-float shares / Total outstanding shares

Suppose Neha is evaluating a company that has 100 crore outstanding shares. Out of these, 35 crore shares are held by promoters and other non-public shareholders, while the remaining 65 crore shares are available for public trading.

Using the formula:

Free-float factor = 65 crore / 100 crore = 0.65

This means that 65% of the company’s shares are available for trading, while the remaining 35% are held by shareholders whose holdings are not typically considered part of the public float.

The higher the free-float factor, the greater the proportion of shares available to public investors in the stock market.

The figures shown are for illustrative purpose only

How to calculate free-float market capitalisation

Free-float market capitalisation represents the value of a company’s shares that are available for public trading. Unlike total market capitalisation, it excludes shares held by promoters, strategic investors, government entities, and other shareholders whose holdings are not typically traded in the market.

You can calculate free-float market capitalisation using either of the following methods.

Formula

Method 1: Using free-float shares

Free-float market capitalisation = Current share price x Number of free-float shares

Method 2: Using the free-float factor

Free-float market capitalisation = Total market capitalisation x Free-float factor

Where:

Free-float factor = Free-float shares / Total outstanding shares

Example

Assume a company has:

| Particulars | Value |

| Total outstanding shares | 20 crore |

| Current share price | ₹ 250 |

| Promoter and strategic holdings | 60% |

| Publicly tradable shares | 40% |

Step 1: Calculate the total market capitalisation

Total market capitalisation = 20 crore x ₹250

= ₹5,000 crore

Step 2: Calculate the number of free-float shares

Since 40% of the shares are available for public trading:

Free-float shares = 20 crore x 40%

= 8 crore shares

Step 3: Calculate the free-float factor

Free-float factor = 8 crore / 20 crore

= 0.40

Step 4: Calculate the free-float market capitalisation

Using Method 1:

Free-float market capitalisation = 8 crore x ₹250

= ₹2,000 crore

Using Method 2:

Free-float market capitalisation = ₹5,000 crore x 0.40

= ₹2,000 crore

The company’s total market capitalisation is ₹5,000 crore. However, because only 40% of its shares are available for trading, its free-float market capitalisation is ₹2,000 crore.

This means ₹2,000 crore represents the value of shares that are actively available to investors in the stock market, making it a more relevant measure for assessing liquidity and index weightage.

The figures shown are for illustrative purpose only

Price-Weighted vs Market-Capitalisation-Weighted Indices: Key Differences Explained

Both methods are used to calculate stock market indices, but they differ in how they assign weight to individual stocks and influence index movements:

| Factor | Price-weighted index | Market-capitalisation-weighted index |

| Basis of weighting | Share price | Market capitalisation |

| Stock influence | Higher-priced stocks carry more weight | Larger companies carry more weight |

| Sensitivity | More sensitive to share price changes | More sensitive to changes in company value |

| Impact of stock splits | Can significantly affect index weightings | Usually has a limited impact |

| Market representation | Reflects movements based on stock prices | Better reflects company size and market value |

| Examples | Dow Jones Industrial Average, Nikkei 225 | Nifty 50, Sensex, S&P 500 |

Significance of free float in the Indian stock market

Understanding free float can help investors better interpret stock liquidity, index movements, and market participation:

- Free float provides a clearer view of the proportion of shares that are available for public trading.

- Investors can use it to assess the potential liquidity of a stock beyond its total market capitalisation.

- Better index representation is achieved by giving greater weight to companies with a larger publicly tradable shareholding.

- Benchmark indices benefit from free-float weighting because it reflects the investable portion of the market.

- Index funds and ETFs rely on free-float data to align their holdings with stocks that are more readily available for trading.

- Comparisons between companies become more meaningful when differences in promoter ownership levels are taken into account.

- The concept is particularly relevant in India, where many listed companies have significant promoter shareholding.

Also Read: What Is a Large Cap? Definition and How to Invest

How stock exchanges use free float to calculate indices

Indian stock exchanges such as the National Stock Exchange (NSE) and the BSE use the free-float market capitalisation methodology for major benchmark indices, including the Nifty 50 and the Sensex.

Under this approach, a company’s weight in an index is determined by its free-float market capitalisation rather than its total market capitalisation. This helps ensure that index weights reflect the shares that are actually available for public trading and investment.

As a result, two companies with similar total market capitalisations may receive different index weights if their free-float levels differ significantly.

Index providers determine free-float factors using publicly available shareholding data. These factors are periodically reviewed and may be revised when ownership structures change due to events such as promoter stake sales, offer-for-sale (OFS) transactions, lock-in expiries, strategic investments, or other changes in shareholding patterns.

For investors in index funds and ETFs, portfolio allocations are generally based on these free-float-adjusted index weights, helping the funds track their benchmark indices more closely.

Relationship between free float size and stock volatility

Free float can influence how easily a stock is traded in the market, which may in turn affect price movements.

Companies with larger free floats may experience relatively smoother price discovery because a greater number of shares are available for trading. This can make it easier for buyers and sellers to transact without significantly affecting the stock price.

Conversely, companies with smaller free floats may witness sharper price movements when demand or supply changes. With fewer shares available for trading, even relatively small buy or sell orders can have a larger impact on market prices.

However, free float alone does not determine a stock’s volatility. Price movements may also be influenced by factors such as:

- Earnings announcements

- Sector-wide developments

- Institutional investor flows

- Corporate governance developments

- Broader market sentiment

- Trading activity and liquidity conditions

While free float can influence liquidity and trading dynamics, volatility remains dependent on a combination of company-specific and market-wide factors.

Benefits of free-float market capitalisation for investors

Free-float market capitalisation can offer useful insights when evaluating stocks and understanding market dynamics:

Better liquidity assessment

It helps investors understand how many shares are actually available for trading in the market.

More meaningful stock comparisons

It allows investors to compare companies with similar market capitalisations but different levels of publicly tradable shares.

Improved understanding of index weightage

It explains why certain stocks receive a higher weight in benchmark indices such as the Nifty 50 and Sensex.

Enhanced evaluation of trading activity

It provides additional context on how share availability may influence trading volumes and market participation.

Support for passive investing

It helps investors understand how index funds and ETFs allocate their investments based on free-float-adjusted weights.

Reduced valuation misinterpretation

It prevents investors from assuming that a large market capitalisation automatically translates into a large number of tradable shares.

Also Read: Index vs Large Cap Funds: Key Differences Explained

Conclusion

Free-float market capitalisation focuses on the shares of a company that are actually available for public trading, offering a more practical view of its tradable market value. Unlike total market capitalisation, which includes all outstanding shares, it reflects the portion of a company’s shares that investors can actively buy and sell in the market.

This methodology plays an important role in index construction in India and influences how benchmark indices such as the Nifty 50 and Sensex are weighted. By understanding free float, investors can better assess factors such as liquidity, index weightage, and the availability of shares for trading.

Evaluating both total market capitalisation and free-float market capitalisation can provide a more complete understanding of a company’s market presence and trading characteristics.

FAQs

What is free-float market capitalisation?

Free-float market capitalisation is the market value of a company’s shares that are available for public trading on a stock exchange. It excludes shares held by promoters, strategic investors, government entities, and other shareholders whose holdings are not regularly traded.

How is free-float market capitalisation calculated?

Free-float market capitalisation is calculated by multiplying the current share price by the number of free-float shares. It can also be calculated by multiplying a company’s total market capitalisation by its free-float factor.

What is the difference between free float and outstanding shares?

Outstanding shares include all shares issued by a company, regardless of who owns them. Free-float shares include only the shares that are available for public trading in the stock market.

Does a higher free float mean lower volatility?

Not necessarily. While a higher free float may improve liquidity and support smoother price discovery, stock volatility is also influenced by factors such as market sentiment, trading activity, earnings announcements, and investor behaviour.

Which shares are excluded from free-float calculation?

Free-float calculations typically exclude shares held by promoters, founders, strategic investors, certain government entities, employee welfare trusts, and shares subject to lock-in restrictions. These shares are generally not considered readily available for public trading.